Assoc Prof Evan Jones provided a case study, which show the Kafkaesque way the banking industry taunts, tortures and rorts its victims — and allows no recourse.

[Read Part One]

[Read Part Two]

[Read Part Three]

THE WINTON TORMENT

THE COMMONWEALTH BANK of Australia bought BankWest from its struggling parent HBOS in October 2008, albeit having to wait until December for formal legitimation of the purchase by the federal Government. The CBA immediately set in train the default and foreclosure of myriad small developers and hoteliers, mostly in Queensland and New South Wales, estimated to be almost 1,000 in number. Indeed, BankWest had intermittently begun corrupt defaults before the takeover.

One of that number was Ken Winton, a NSW builder with 35 years experience, having learnt the trade from his father. His story has been summarised in Part III of my The Dark Side of the Commonwealth Bank. It is worth revisiting the Winton story as a case study in the CBA takedown. The following is drawn partly from the Ken Winton submission to the current Senate Committee post-GFC banking Inquiry, #148. With variations on a common theme, there are hundreds more like it.

The Winton story is chosen here because the Senate Committee Secretariat invited responses from the institutions that Winton complained about in his submission. We thus have a Rashomon-type scenario with conflicting accounts of the same phenomenon. This account will eschew filmmaker Kurosawa’s impartiality, opting for a partisan interpretation of the events.

There is a sizeable cabal that initiated or facilitated the destruction of a viable business, destroyed the Wintons’ livelihood, and damaged their reputation for the indefinite future. The Wintons obtained bank loans from BankWest totaling almost $4 million for two unit developments in Nambucca Heads, in September 2005 (Parkes St) and March 2007 (Bowra St).

After the CBA takeover, BankWest ordered a valuation from Coffs Harbour-based Magann O’Rourke on 5 November 2008, delivered on 19 November. Winton notes that the valuation was ordered without tender, and the recipient paid twice the conventional fee. Winton claims that the report contained downgraded valuations that were

‘...misleading, grossly unprofessional (the use of hearsay) and have numerous mistakes’.

The next day, Middletons Solicitors issued BankWest’s ‘notice of default and demand’. Without knowing anything more, one can readily infer that this is a corrupt act on the part of BankWest, under the CBA’s direction.

Winton’s lending manager Jim Williams had three multi-unit developer customers on his books. All three had valuers called in, all had their properties substantially devalued, and all were defaulted and foreclosed on. The defaults were manufactured. Williams was moved on in January 2009 (standard bank practice for lending managers in the spotlight). Winton’s new relationship manager (sic), Philip Alcock, settled in by declining to respond to persistent requests for information, clarification and action.

In January 2009, the bank imposed on Winton’s debt a penalty interest rate of 8% over the bill rate, and charged Winton $20,000 for a variation of facilities imposed by the bank itself. By April, the total rate had become 16.6%, creeping up to 18.8% by December 2010. The bank had already imposed a 4% penalty rate in July 2008 on spurious grounds. In September 2009, the Wintons were forced to sell their own (unmortgaged) home, quickly and under value, to reduce the debt mounting under penalty interest charges. The penalty rates were to rip hundreds of thousands of dollars out of Winton’s equity.

With the Wintons’ home sale achieved and the Wintons’ equity garnered, BankWest immediately sent in Rodgers Reidy as receiver and manager to the Winton company, Paoli P/L. BankWest then ceased to remit statements. The statements were henceforth sent to Paoli P/L c/f Credit and Asset Management, the BankWest division for ‘impaired’ loans.

Bizarrely, the statements include the phrase:

‘Your Facility has expired, default interest rates, as set out in your loan contract, will apply as from 22 October 2009. Your immediate action is required.’

It is relevant that the CBA was the subject of a 2000 Joint Committee on Corporations and Financial Services Inquiry for the bank ceasing to issue statements to customers that it had placed in default. The CBA made a commitment to the Parliamentary Committee that it would henceforth continue to issue bank statements to defaulted customers; it failed from word go to honour that commitment.

Winton claims that Rodgers Reidy took no positive action on the sale process for months, and that promising leads for sales were not followed up. With the bank’s penalty interest rate charges accumulating, Winton inferred that the receiver’s inaction was a vehicle for the bank to siphon off Winton’s equity in Paoli. Meanwhile, Middletons, simultaneously claiming to be the sole vehicle of communication between the parties, but itself refusing to communicate, wrote to Winton to instruct him to stop writing letters of complaint to the bank or to the receivers.

In January 2010 (albeit claiming an earlier date), Rodgers Reidy began preparations for sale of the Paoli units, delegating Ray White Nambucca Heads. The units were initially advertised wrongly as subject to ‘mortgagee in possession’ (a vehicle to push prices down). The first unit (151 sq.m.) was sold under value in February for $360,000. The pre-existing purchaser of unit 6 immediately cancelled his contract for $525,000. Unit 6 was sold belatedly in August for $342,000.

In March 2010, Winton lodged a complaint with the Financial Ombudsman Service (FOS).

In May, Winton wrote to the CEO and Board of the CBA complaining about Alcock’s unresponsiveness to letters from Winton (and failure to pass correspondence to his superiors). CBA Board member David Turner had replaced the seemingly useless John Schubert as CBA Chairman in February 2010, but it was evidently to be business as usual. The CBA passed Winton’s complaints to BankWest’s External Dispute Resolution Service Quality Coordinator (sic) who replied belatedly in July that “the matters you raise appear to be queries which should be properly directed to the receiver” and “I respectfully request you please send any further correspondence to Mr Wyhoon of Middletons Solicitors”.

Meanwhile, Middletons continued to deflect Winton’s entreaties with 'our clients do not intend to respond in detail to any further correspondence …', claiming we 'continue to deny any improper conduct”'. In August, BankWest writes that it is keeping Paoli in receivership and, in September, reiterates that all correspondence has to go through Middletons.

In September, Winton lodged a complaint with the Australian Securities & Investments Commission (ASIC). In October, BankWest’s Customer Advocacy Manager (sic) wrote that the bank was ‘comfortable’ that the complaint was in the hands of the FOS. In November (eight months after Winton made a complaint), the FOS claimed that it hadn’t got on to Winton’s case as things were busy.

Revenue from the last of the properties sold was not booked until November 2010. In October Rodgers Reidy had advised ASIC that it expected to hold Paoli in administration for a further 12 months. In November, Winton complained to the Insolvency Practitioners Association (IPA), the receivers’ industry body, regarding Rodgers Reidy’s modus operandi. The receiver replied to Winton, denying his allegations. It also noted:

“We are now in a position to finalise the matter and subsequently retire from our appointment.”

In December, Winton paid to obtain Rodgers Reidy's ASIC returns. For Winton, the information was inadequate and contained discrepancies. For example, the first four units sold have the purchasers’ names listed upon receipt of funds in March 2010. The names of purchasers of units sold after late March are not recorded on the receiver’s returns. Did the receiver have something to hide?

Winton complained again to the IPA of Rodgers Reidy’s operations. In early January 2011, the receiver replied with: “we continue to deny the various allegations in your letters” and “your letters add to the cost of the receivership”, but promising ready relinquishment of its administration.

In December 2010, Winton had written again to the CEO and Board of the CBA regarding non-cooperation or compliance of all relevant parties. The CBA again handed the complaint to BankWest, which replied: “it does not appear there is any substance to your complaints”; and, a week later:

“...the Bank remains of the view that it has not breached the legislation you refer in your letters.”

In January 2011, Winton wrote yet again to the CEO and Board of the CBA, as well as to the IPA (twice), requesting intervention. For a third time, the CBA passed the matter down to its subsidiary, with BankWest replying “the Bank remains of the view that it has not breached the legislation you refer” (Winton made constant references to the Corporations Act).

In February, Winton wrote a fourth, fifth and sixth time to the CEO and Board of the CBA (same shifting of responsibility and same response from BankWest), and again to the IPA. Winton wrote a seventh time to the CBA in March and again in April, demanding to know why all previous requests for the assumption of responsibility for his case had been ignored.

In March, Rodgers Reidy disclosed to Winton that they can’t hand back the company yet because they had issues with the Tax Office to resolve.

Also in March, Winton wrote to ASIC requesting access to the material for his company that Rodgers Reidy had lodged with ASIC. ASIC replied (Winton had complained to them in September 2010) that “this matter is taking longer than we expected”. Both the FOS (in possession of Winton’s complaint for 12 months) and ASIC replied that they might get around to his case sometime. In April, ASIC wrote again, noting (without a hint of irony):

“...ASIC is looking at your complaint in conjunction with similar complaints from other people”

and

“...ASIC’s decision to take action will be influenced by whether there is evidence of systemic concerns, and whether it is in the public interest to take action, after the consideration of all relevant concerns.”

In April, Winton noted to ASIC that ASIC itself had imposed an enforceable undertaking in May 2007 on a previous partner of Rodgers Reidy, the partner having engaged in a number of unconscionable practices. Yet here was Winton complaining about Rodgers Reidy engaging in comparable practices, and he was being ignored.

Rodgers Reidy relinquished the receivership of Winton’s company in April 2011, but declined to return to Winton documentation of its administration of Winton’s company. Naturally, Winton would be interested in details like letters of instruction to Ray White R/E, invoices from Middletons, correspondence with Partridge Partners, correspondence with the property purchasers, and so on.

Rodgers Reidy had paid itself $208,000 for its administration, and had paid Middletons $167,000. The Middletons' payment constitutes effectively $16,000 conveyancing fee for each of the 11 units sold ― whereas a typical conveyancing fee is around $1,500 to $2,000. Included in the total fee was a $53,000 charge for three units sold in one line to one purchaser.

In May, the IPA belatedly responded by affirming that the IPA does not uphold Winton’s complaint against Rodgers Reidy personnel, also claiming that “it is not the IPA’s role to assess the commercial and professional judgement” of such personnel ― a contradictory stance, as the IPA has clearly assessed Rodgers Reidy personnel as having no case to answer. Winton responded to the IPA noting that the IPA’s website discloses its accepted regulatory responsibility – vide:

‘The IPA has powers to investigate complaints against members in relation to their professional conduct as a practitioner. Complaints are important and will be properly dealt with.’

In July, ASIC wrote to say that “ASIC has decided not to take any further action at this time”. Winton replied that, by ASIC’s own criteria, one couldn’t anything more systemic than the treatment accorded to CBA/BankWest victims like himself.

In early August, the FOS wrote to note that they accepted the investigation (Winton had complained to the FOS in March 2010, 17 months previously). In late August, the FOS wrote to claim that Winton’s complaint was outside its jurisdiction, as the bank’s figures showed a residual debt of over $800,000 but the FOS is only ‘able to consider a dispute where the value of the applicant’s claim is up to $500,000’. Winton replied to the FOS in September (and again in January 2012) arguing that more accurate figures put his dispute within the FOS limit for consideration. But the fact is that Winton was being ripped off to the tune of $1 – 2 million, and the FOS (as noted below) is a bottomless pit of self-satisfied irrelevance that has diverted the energies of CBA/BankWest and other victims.

In October 2011, ASIC confirmed that it would not handle Winton’s complaint, and that if he didn’t like it he should go to the Commonwealth Ombudsman. Which Winton did. The Ombudsman stuffed around for two months, asking for further information, only in early December to note that I “have made the decision not to investigate your complaint”.

In December, the FOS wrote to claim:

'While I accept that the information contained in the Receiver’s statements does not exactly match the amount owing to Bankwest, it is not the role of this office to investigate that discrepancy.'

Correspondence to the FOS from BankWest (dated 8 November) claimed to reconcile the un-reconcilable discrepancy. The BankWest letter (signed by Christopher Aird, Senior Case Manager, Customer Relations) is a rambling joke, demonstrating complete disdain for the lack of clarity of divergent figures and the lack of integrity of the process. In January 2012, Winton wrote to the FOS to demand that it investigate the figures both from the receiver and from BankWest. The FOS replied that it takes BankWest’s figures as gospel (but Rodgers Reidy figures?).

In January 2012, Winton notified the IPA that Rodgers Reidy had still not returned his company’s books. Also in January, the ATO wrote to inform Winton that it had not reviewed Winton’s mid-2011 claims regarding Rodgers Reidy and its GST responsibilities; to date, it still hasn’t.

In February, Winton wrote to the CEO and Board of the CBA relating to the conduct of BankWest, Rodgers Reidy and Middletons, asking why it had not responded directly to his correspondence on ten previous occasions. In March, CBA Customer Relations (sic) emailed to say that Winton’s situation was under review. Meanwhile, BankWest wrote requesting a meeting so that “the parties can make attempts to reach an amicable resolution to ongoing matters”. BankWest dictated that the meeting would be held at Middleton’s offices and that Winton’s request to bring along the principals of the BankWest activist group Unhappy Banking could not be accommodated.

Under these conditions, Winton declined to agree to a meeting.

Eventually, the CBA emailed again to reiterate that BankWest was the appropriate vehicle to deal with Winton’s concerns. The CBA General Manager Group Customer Relations claimed:

'If you are unhappy with Bankwest’s response to your complaint, you can contact the Financial Ombudsman Service, a free and independent resolution service.'

Winton pointed out to the Inquiry Committee that the said author of this recommendation, Brendan French, was himself a Board member of the FOS.

And so it goes.

If the preceding paragraphs have induced a state of ennui in the reader, they encapsulate a nightmare scenario for the Wintons that began in November 2008 and is still in play. The scenario depicted in the Ken Winton submission is Kafkaesque. Googling this latter term suggests an atmosphere ‘marked by a senseless, disorienting, often menacing complexity.’ Kafka biographer Frederick Karl elaborates:

What's Kafkaesque is when you enter a surreal world in which all your control patterns, all your plans, the whole way in which you have configured your own behavior, begins to fall to pieces, when you find yourself against a force that does not lend itself to the way you perceive the world. You don't give up, you don't lie down and die. What you do is struggle against this with all of your equipment, with whatever you have. But of course you don't stand a chance. That's Kafkaesque.

Of course, Kafkaesque situations are the product of fiction, dreamt up by a warped mind ― or, at worst, generated by primitive oppressive regimes somewhere in Eastern Europe. No, they are present in modern enlightened Australia, certainly dreamt up by warped minds and courtesy of oppressive regimes engineered by our bastard banks.

Ken Winton’s listing of his tormentors in his submission led the Senate Committee Secretariat to invite the accused to respond to the calumny perpetrated against their good reputations. They are placed on the Committee’s submission list directly below Winton’s submission.

First the IPA.

The IPA claims that

“We investigated the complaint and did not find, on the information we had, that there was any issue of misconduct.”

Yet, in May 2011, the IPA had claimed to Winton “it is not the IPA’s role to assess the commercial and professional judgement” of its members.

The IPA response claims that the receiver (under the IPA code)

“...owes a primary duty to the creditor – in this case it was BankWest – under the terms of its appointment.”

So the IPA condones a manufactured default, a questionable administration of a bank customer’s assets and the corrupt appropriation and disbursement of those assets to various predators. Contemptible, and complicit.

The receiver was hired to secure BankWest’s (artificially inflated) debt, and the receiver thus, the IPA claims, had obligations to the bank that hired it (albeit the victim borrower pays the bill). It is instructive to hear a learned member of the bench discourse on this very subject. This from Spender J in NAB v Freeman, Federal Court of Australia (Brisbane) 244, 12 March 2002.

20 This claim asserts that the conduct of the receiver appointed by the bank in selling Mr Freeman's property exposed the bank to a liability at Mr Freeman's hands for negligence in the conduct of that sale. The short answer by the bank is that, pursuant to the mortgage, the receiver was the mortgagor's [the borrower’s] agent and so any claim that Mr Freeman has is against the receiver as his principal, and that that claim does not assist him as against the bank. That involves a consideration of the efficacy of the term of the mortgage by which the parties agreed (using the somewhat artificial meaning of agreement when a mortgagor is presented by a mortgagee with a mortgage to sign) which provides that the receiver appointed by the mortgagee [the bank] is the agent of the mortgagor.

21 The unreality of that situation in fact is a matter which has troubled me on a number of occasions, but the authorities to which I will refer make it plain that I ought to accept that the contractual term is effective, so that the receiver appointed by the mortgagee, exercising the power expressed in the bill of mortgage, is acting as agent for the mortgagor. Notwithstanding what might be thought the unreality of the situation, the legal position is that, if there was negligence in the conduct of the sale, Mr Freeman would have an action against the receiver. Almost certainly, the receiver will have received an indemnity from the bank, but the legal characterisation of his rights in respect of any claimed sale at an undervalue is legally a claim against the receiver and not against the bank.

22 I should refer to a number of authorities which touch on this question. …

In two paragraphs there is displayed, in all its Kafkaesque clarity, the utter bankruptcy and corruption of the Australian legal system. The borrower signatory to a mortgage has not ‘agreed’ to its terms but is forced to sign, and in spite of ‘what might be thought the unreality of the situation’, legal precedent delivers the verdict to the bank on a plate. Any incompetence and crimes of the receiver do not implicate the bank that hired and directed the receiver, but must henceforth be a matter for pursuit by the victim, soon-to-be-penniless, borrower. Brilliant.

Second, the receivers Rodgers Reidy.

The Rodgers Reidy response is a polar opposite account to that of Winton’s. It is detailed, and prima facie compelling. Who to believe? The busy Senators and Committee Secretariat may find details too forbidding to delve further. The Secretariat and the Senators may think, phew, these defaulted BankWest developers had it coming. But some elements in the receiver’s response, in conjunction with its ASIC returns, are curious.

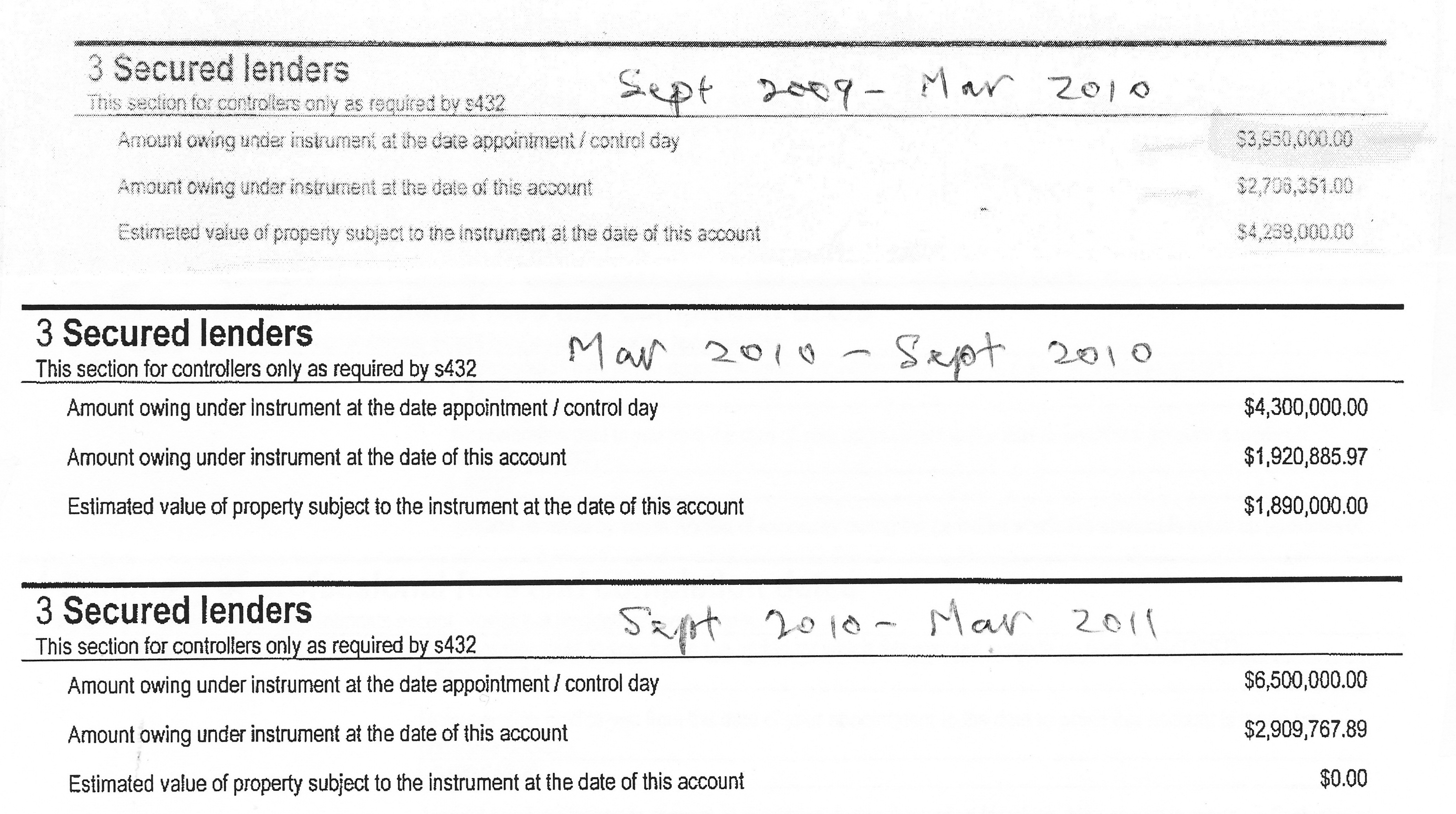

Receivers are required to submit to ASIC a ‘524’ form every six months enclosing the details of the administration of a company in receivership. Rodgers Reidy ran the Paoli receivership between September 2009 and April 2011, submitting three 524 forms – for March 2010, September 2010 and March 2011. A bank statement dated 19 September 2009 has the debt at the time of appointment of the receiver at $4,414,462. (Net funds from sale of the Winton residence, $723,000, were banked in October, reducing the claimed debt to $3,691,462.) The receiver’s first 524 return has the debt at foreclosure at $3,950,000. The second 524 return to ASIC has the debt at foreclosure at $4,300,000; the third 524 return has the debt at foreclosure at $6,500,000. What?

As noted above, Winton sought clarification via the FOS of the divergence in the debt balance between the bank statement and Rodgers Reidy’s first report. BankWest’s letter to the FOS, dated 8 November 2011, reports that Rodgers Reidy claims that its figure included

'...estimated agency fees and legal fees which would be necessarily incurred to realise the assets under the control of the receiver.'

Gobbledegook.

The bank adds:

'...the figure in the form 524 would also include an amount for accrued interest.'

That claim is rubbish for the first return figure of $3,950,000, but plausible for the second return figure (six months later) of $4,300,000. The 524 forms are flawed in that there is no place for the recognition of accrued interest, which the receiver is ignoring and which is being capitalised into the total debt figure. The debt at foreclosure is thus a moveable feast, which can be turned into any figure that the bank desires, by upping the penalty interest rate and dragging out the foreclosure period.

Then there is the third return $6,500,000 figure ― a preposterous, over the top, a transparent fabrication.

A resulting, striking, anomaly is Winton’s final balance with BankWest.

The BankWest facility statement has Winton’s final debt as at December 2010 (after sale of all properties) at $781,000. An email from the Winton’s manager to Noelene Winton on 25 January 2011 notes (the sole content of the email): ‘The Balance of the facility still outstanding/owing as at 8th December 2010 was $769,526.04 plus interest and fees.’ The same date, two different figures. No statement was supplied by Alcock to accompany this email, and the Wintons did not obtain copies of their bank statements until later. The Rodgers Reidy third return has the Wintons’ final debt at $2,909,767. That fanciful figure is presumably some kind of residual outcome from the fabricated $6,500,000 debt at time of default.

To add to the chaos, the 8 December bank statement also has the $781,000 debit balance written down as an ‘Account Closing Entry’, leading to a ‘Closing Balance’ of 0.00! Has the debt been moved to a Shadow Ledger account, or has it been written off? The 25 January 2011 email implies that the (contrived) debt has not been written off. The Tax Office would know, but it’s not saying.

So what is the final outcome of the Wintons’ relationship with BankWest? The bank has not tried to bankrupt them, but BankWest has ceased communication, and the Wintons’ final status remains unknown and unresolved. In an article in the Australian Financial Review (by its Western Australian correspondent Natalie Gerritsen), 9 February 2012, it is reported: ‘A Bankwest spokeswoman says talks are continuing with Winton to resolve the situation’, involving ‘ongoing discussions’.

The spokeswoman is simply lying.

In its response to Winton’s Inquiry submission, Rodgers Reidy claims that a series of impasses prevented it from expediting sales. First, there were missing fittings ― carpets, blinds, hot water systems, cabinetry. Well of course, says Winton ― it is conventional to install these fittings only after a contract for sale has been established. More significant, Rodgers Reidy claims that the Bowra St building had major structural defects. A report was ordered on or around 21 January 2010, which (according to Rodgers Reidy) claimed that necessary repairs would be of the order of $200,000.

The marketing campaign is claimed to have begun on 3 December 2009. Why did there occur a lapse of 4 months before such a report was solicited, given that these ‘major’ structural faults would have been self-evident? Rodgers Reidy also claims that the Council was not satisfied with the condition of the building. Then where are the rectification notices from Council, and the disclosure to potential purchasers of non-compliance?

The most significant dimension of the 524 reports is the listing of receipts and payments during the relevant period. Payments expended to subcontractors for the entire receivership period totaled $35,200, the bulk clearly for unit fit-out. Within the $35,000 is a payment of $3,700 to Partridge Partners on 4 February 2010, labeled ‘subcontractors’. Is this payment for repair work or mislabeled as a payment for the damning report? There is no listed payment for the damning report. Moreover, there is no evidence of payment for the remediation of significant structural flaws. Have the unit purchasers been knowingly sold lemons? Or is there another explanation for the anomalies?

Rodgers Reidy claims that

‘… we retired from this appointment on 11 April 2011. Finalisation of the matter was delayed by 3-4 months as a result of the difficulties encountered in obtaining BAS documentation from the ATO and finalising the Company’s taxation position.’

Well no. Rodgers Reidy apparently failed to pay on time the GST associated with unit sales (a neglect widespread in the receiver sector, with the associated financial advantages); all GST payments were made in late October and November 2010, over six months after completion of some sales. As a consequence, Rodgers Reidy was fined over $8,100 for the late lodgement. Rodgers Reidy appealed to the ATO and the fine was wavered.

Rodgers Reidy completes its response by claiming that

‘All books and records of the Company were subsequently returned to Mr Winton.’

Well no they weren’t. And so on.

Third, the Financial Ombudsman Service.

The FOS response to the Winton submission, under Chief Ombudsman (ex-ASIC) Shane Tregillis’ signature, is a masterpiece of managerialist obfuscation. There is a comparable vacuous response by the FOS to Gregory Cadwallader’s Senate Inquiry submission, #11.

Tregillas claims that the FOS has ‘extensive obligations in regard to systemic issues’, and that ‘We provide comprehensive reports to ASIC on systemic issues’.

Where is the evidence? Cadwallader was a victim of systemic corruption within the ‘wealth management’ business of the CBA’s Commonwealth Financial Planning Limited, but neither the FOS nor ASIC acknowledged the systemic problem. Winton is a victim of systemic corruption resulting from the CBA’s takeover of BankWest, and associated systemic corruption within the receiver industry, but neither the FOS nor ASIC are prepared to join the glaring dots.

Winton’s allegations that the FOS is not independent of its financial provider backers is answered by Tregillis saying that the FOS ticks all the boxes of ASIC’s Regulatory Guide 139. Kafka where are you? The answers to Winton’s (and Cadwallader’s) allegation resides not in FOS’s statutory obligations, but in a systematic examination of FOS decisions.

The FOS stuffed Winton around for 17 months before telling him to bugger off. He doesn’t fall within their $500,000 upper limit for disputes, they said. Even if true, they could have told him that within a week. But the problem of a financial limit to FOS’ jurisdiction goes much deeper.

In its earlier incarnation as the Banking Ombudsman, the organisation was restricted to a mediation role on small scale retail banking complaints. Commercial dealings were outside its bailiwick. In this guise, it worked reasonably well. Latterly, the organisation has acquired greater ‘responsibilities’, but it is structurally incapable of catering to them. It is financed by the institutions who are the subject of complaints to the FOS. Moreover, it cannot handle complaints against organisations outside the fold (lawyers, receivers) that do the bidding of financial institutions.

The FOS is structurally incapable of dealing with financial institution corrupt practices that are systemic. FOS staff appear incapable of confronting the very concept of systemic corrupt practices. Its brief now overlaps with the central role of ASIC, confusing victims as to appropriate avenues for seeking redress, and partially absolving ASIC for its own profound inaction. Mediation may be appropriate when incompetence is involved, but not when corruption is involved. In short, the FOS is a waste of time and resources. Rather than a vehicle for the maintenance of integrity in the financial system it is a vehicle for the opposite.

One can be thankful to the Senate Committee Inquiry for eliciting the details of this story. In this escapade of banks and their hangers-on, one is reminded of the Milgram experiment of the early 1960s, devised by Yale University’s Stanley Milgram. The volunteers in the experiment proved themselves to be prepared to administer electric shocks to strangers because they had been given the authority to do so. Here receivers, lawyers, and so on, show themselves prepared to torture bank customers because they have been given the authority by bank management to do so. In turn, bank managers show themselves prepared to torture bank customers and to delegate authority for same to their agents because they have been de facto granted authority by financial regulators, the legal system and the political class itself. And the torturers get to plunder the customer’s bank account to garnish the sadism.

The Milgram experiment ended in controversy. But the process described above has been legitimised as an integral element of white collar professional life. The Commonwealth Bank of Australia is a past master of the art. White collar crime, that seeming oxymoron and blood sport of the fortunate, is the subject of the concluding instalment in this series, to be published in the next few days.

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivs 3.0 Australia License

{kind=link}

{kind=link}

{kind=link}